Page 13 - BoAML Plan Handbook 17 V2.0

P. 13

Sample contribution calculation Tax-efficient saving limits

The following examples are based on 2017/18 tax and National Insurance contribution rates. The Annual Allowance Lifetime Allowance

The Annual Allowance (AA) is the maximum total contribution The Lifetime Allowance (LTA) is the total value of pension

that can be paid into your pension plan(s) in one tax year by savings you can build up tax efficiently during your lifetime.

Laura, 24, a basic-rate tax payer, Tom, 45, a higher-rate tax payer,

has a Plan Salary of £20,000. has a Plan Salary of £50,000. you and your employer, without incurring a tax charge. If the The ‘test’ of your savings against the LTA starts to be carried

She has worked at your employer He has worked at your employer contribution paid to your pension plan(s) is more than the AA, out at the time you begin to use your savings.

for three years. for 11 years. you will pay income tax on the excess at your marginal rate. For the 2017/18 tax year, the LTA is £1 million.

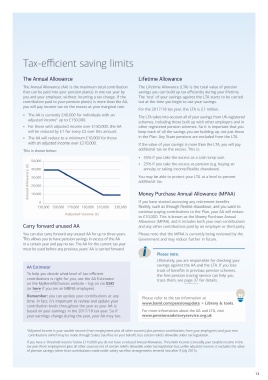

• The AA is currently £40,000 for individuals with an The LTA takes into account all of your savings from UK-registered

3% 3% adjusted income* up to £150,000.

Laura decides to pay 3% of her Plan Salary. Tom decides to pay 3% of his Plan Salary. schemes, including those built up with other employers and in

• For those with adjusted income over £150,000, the AA other registered pension schemes. So it is important that you

Her gross pay would reduce by £600 a year. His gross pay would reduce by £1,500 a year. will be reduced by £1 for every £2 over this amount. keep track of all the savings you are building up, not just those

£600 £1,500 • The AA will reduce to a minimum £10,000 for those in the Plan. Any State pensions are excluded from the LTA.

The cost to Laura is just £408 a year (in The cost to Tom is just £870 a year (in with an adjusted income over £210,000.

terms of take-home earnings) and with your terms of take-home earnings) and with your If the value of your savings is more than the LTA, you will pay

employer's contribution of 8% (£1,600)... employer's contribution of 12% (£6,000)... This is shown below: additional tax on the excess. This is:

£1,600 £6,000

...a total of £2,200 a year would go into ...a total of £7,500 a year would go into 50,000 • 55% if you take the excess as a cash lump sum.

Laura’s Member Account. Tom’s Member Account. • 25% if you take the excess as pension (e.g. buying an

Annual Allowance (£) 30,000 You may be able to protect your LTA at a level to prevent

= £2,200 = £7,500 40,000 annuity or taking income/flexible drawdown).

additional tax.

20,000

Please note: Please note: 10,000 Money Purchase Annual Allowance (MPAA)

• The contributions your employer makes to Tax rates, tax relief and National Insurance

your Member Account are based on your Plan contribution rates may vary in line with 0 If you have started accessing any retirement benefits

Salary before any reduction for your additional legislation. The value of tax relief will depend 130,000 150,000 170,000 190,000 210,000 230,000 flexibly, such as through flexible drawdown, and you want to

contributions. This also applies for any other on your personal circumstances and when you Adjusted income (£) continue paying contributions to the Plan, your AA will reduce

tax-efficient benefit choices you make through make your contributions. to £10,000. This is known as the Money Purchase Annual

MyBenefitChoices. Carry forward unused AA Allowance (MPAA), and it includes both your own contributions

and any other contributions paid by an employer or third party.

• Any contributions you make through Salary

Sacrifice are considered as bank contributions. You can also carry forward any unused AA for up to three years. Please note that the MPAA is currently being reviewed by the

More information about how this impacts This allows you to have pension savings in excess of the AA Government and may reduce further in future.

your options if you leave the Plan is set out in a certain year and pay no tax. The AA for the current tax year

on page 32. must be used before any previous years’ AA is carried forward.

Please note:

• The reduction made to your basic salary through

Salary Sacrifice will not affect any other Ultimately, you are responsible for checking your

salary-related payments or savings that you AA Estimator savings against the AA and the LTA. If you lose

receive from your employer, such as salary To help you decide what level of tax-efficient track of benefits in previous pension schemes,

increases, bonuses and overtime, or any of contributions is right for you, use the AA Estimator the free pension tracing service can help you

the benefits payable on death or retirement. on the MyBenefitChoices website – log on via SSO trace them; see page 37 for details.

(or here if you are an MBNA employee).

Remember: you can update your contributions at any Please refer to the tax information at

time. In fact, it’s important to review and update your www.baml.com/pensionupdate > Library & tools.

contribution levels throughout the year as your AA is

based on your earnings in the 2017/18 tax year. So if For more information about the AA and LTA, visit

your earnings change during the year, your AA may too. www.pensionsadvisoryservice.org.uk

* Adjusted income is your taxable income (from employment plus all other sources) plus pension contributions from your employer(s) and your own

contributions (which may be made through Salary Sacrifice on your behalf), less certain reliefs allowable under tax legislation.

If you have a ‘threshold income’ below £110,000 you do not have a reduced Annual Allowance. Threshold income is broadly your taxable income in the

tax year (from employment plus all other sources) net of certain reliefs allowable under tax legislation but, unlike adjusted income, it excludes the value

of pension savings (other than contributions made under salary sacrifice arrangements entered into after 9 July 2015).

12 13