Page 203 - Office Practice and Accounting -9

P. 203

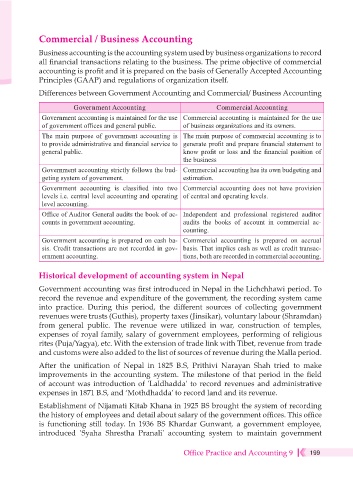

Commercial / Business Accounting

Business accounting is the accounting system used by business organizations to record

all financial transactions relating to the business. The prime objective of commercial

accounting is profit and it is prepared on the basis of Generally Accepted Accounting

Principles (GAAP) and regulations of organization itself.

Differences between Government Accounting and Commercial/ Business Accounting

Government Accounting Commercial Accounting

Government accounting is maintained for the use Commercial accounting is maintained for the use

of government offices and general public. of business organizations and its owners.

The main purpose of government accounting is The main purpose of commercial accounting is to

to provide administrative and financial service to generate profit and prepare financial statement to

general public. know profit or loss and the financial position of

the business

Government accounting strictly follows the bud- Commercial accounting has its own budgeting and

geting system of government. estimation.

Government accounting is classified into two Commercial accounting does not have provision

levels i.e. central level accounting and operating of central and operating levels.

level accounting.

Office of Auditor General audits the book of ac- Independent and professional registered auditor

counts in government accounting. audits the books of account in commercial ac-

counting.

Government accounting is prepared on cash ba- Commercial accounting is prepared on accrual

sis. Credit transactions are not recorded in gov- basis. That implies cash as well as credit transac-

ernment accounting. tions, both are recorded in commercial accounting.

Historical development of accounting system in Nepal

Government accounting was first introduced in Nepal in the Lichchhawi period. To

record the revenue and expenditure of the government, the recording system came

into practice. During this period, the different sources of collecting government

revenues were trusts (Guthis), property taxes (Jinsikar), voluntary labour (Shramdan)

from general public. The revenue were utilized in war, construction of temples,

expenses of royal family, salary of government employees, performing of religious

rites (Puja/Yagya), etc. With the extension of trade link with Tibet, revenue from trade

and customs were also added to the list of sources of revenue during the Malla period.

After the unification of Nepal in 1825 B.S, Prithivi Narayan Shah tried to make

improvements in the accounting system. The milestone of that period in the field

of account was introduction of 'Laldhadda' to record revenues and administrative

expenses in 1871 B.S, and ‘Mothdhadda’ to record land and its revenue.

Establishment of Nijamati Kitab Khana in 1925 BS brought the system of recording

the history of employees and detail about salary of the government offices. This office

is functioning still today. In 1936 BS Khardar Gunwant, a government employee,

introduced 'Syaha Shrestha Pranali' accounting system to maintain government

Office Practice and Accounting 9 199