Page 21 - gmj150-Jan-Mar-web-Neat

P. 21

wouldn’t have had this opportunity,” Hyde

said. “But we are experienced operating

there, we understand the risk and can

make the most of the opportunity.”

With the feasibility study complete, WAF

has set out on the financing journey for

Kiaka. Hyde said the debt landscape

has shifted since the company arranged

Sanbrado’s financing in 2018.

“The market has changed in the last few

years, there are a lot more African banks

and investment funds interested,” he

said. “That is kind of refreshing because

it means we don’t have to start every

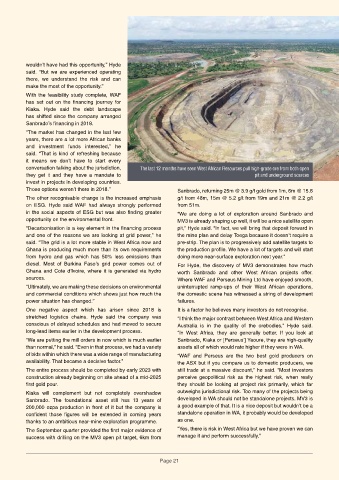

conversation talking about the jurisdiction, The last 12 months have seen West African Resources pull high-grade ore from both open

they get it and they have a mandate to pit and underground sources

invest in projects in developing countries.

Those options weren’t there in 2018.” Sanbrado, returning 25m @ 3.9 g/t gold from 1m, 6m @ 15.6

The other recognisable change is the increased emphasis g/t from 48m, 15m @ 5.2 g/t from 19m and 21m @ 2.2 g/t

on ESG. Hyde said WAF had always strongly performed from 51m.

in the social aspects of ESG but was also finding greater “We are doing a lot of exploration around Sanbrado and

opportunity on the environmental front. MV3 is already shaping up well, it will be a nice satellite open

“Decarbonisation is a key element in the financing process pit,” Hyde said. “In fact, we will bring that deposit forward in

and one of the reasons we are looking at grid power,” he the mine plan and delay Toega because it doesn’t require a

said. “The grid is a lot more stable in West Africa now and pre-strip. The plan is to progressively add satellite targets to

Ghana is producing much more than its own requirements the production profile. We have a lot of targets and will start

from hydro and gas which has 50% less emissions than doing more near-surface exploration next year.”

diesel. Most of Burkina Faso’s grid power comes out of For Hyde, the discovery of MV3 demonstrates how much

Ghana and Cote d’Ivoire, where it is generated via hydro worth Sanbrado and other West African projects offer.

sources. Where WAF and Perseus Mining Ltd have enjoyed smooth,

“Ultimately, we are making these decisions on environmental uninterrupted ramp-ups of their West African operations,

and commercial conditions which shows just how much the the domestic scene has witnessed a string of development

power situation has changed.” failures.

One negative aspect which has arisen since 2018 is It is a factor he believes many investors do not recognise.

stretched logistics chains. Hyde said the company was “I think the major contrast between West Africa and Western

conscious of delayed schedules and had moved to secure Australia is in the quality of the orebodies,” Hyde said.

long-lead items earlier in the development process. “In West Africa, they are generally better. If you look at

“We are putting the mill orders in now which is much earlier Sanbrado, Kiaka or [Perseus’] Yaoure, they are high-quality

than normal,” he said. “Even in that process, we had a variety assets all of which would rate higher if they were in WA.

of bids within which there was a wide range of manufacturing “WAF and Perseus are the two best gold producers on

availability. That became a decisive factor.” the ASX but if you compare us to domestic producers, we

The entire process should be completed by early 2023 with still trade at a massive discount,” he said. “Most investors

construction already beginning on site ahead of a mid-2025 perceive geopolitical risk as the highest risk, when really

first gold pour. they should be looking at project risk primarily, which far

Kiaka will complement but not completely overshadow outweighs jurisdictional risk. Too many of the projects being

Sanbrado. The foundational asset still has 13 years of developed in WA should not be standalone projects. MV3 is

200,000 ozpa production in front of it but the company is a good example of that. It is a nice deposit but wouldn’t be a

confident those figures will be extended in coming years standalone operation in WA, it probably would be developed

thanks to an ambitious near-mine exploration programme. as one.

The September quarter provided the first major evidence of “Yes, there is risk in West Africa but we have proven we can

success with drilling on the MV3 open pit target, 6km from manage it and perform successfully.”

Page 21