Page 33 - pd294-June21-mag-web_Neat

P. 33

Antipa in good company

espite the nearby Telfer

Dmine being one of the

State’s largest, when An-

tipa Minerals Ltd arrived and

pegged in excess of 5,000sq

km of ground 10 years ago,

Western Australia’s Paterson

Province was a lonely place.

As first kids on the block,

Antipa staked prime territory in

what has since become a pop-

ular hunting ground for copper

and gold explorers.

Early works by Antipa –

highlighted by a 370m deep

intersection boasting big ton-

nage potential at Citadel – did

not go unnoticed, with Rio

Tinto Ltd quickly signing up to

a JV.

Initiating its own search

around Antipa’s holdings,

Rio Tinto’s efforts have so

far culminated in an inferred

resource of 503mt @ 0.45%

copper equivalent (0.2% cut-

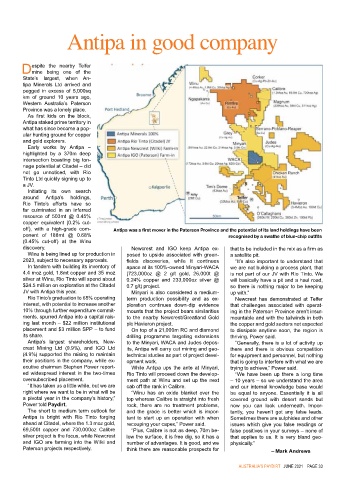

off), with a high-grade com- Antipa was a first mover in the Paterson Province and the potential of its land holdings have been

ponent of 188mt @ 0.68% recognised by a swathe of blue-chip outfits

(0.45% cut-off) at the Winu

discovery. Newcrest and IGO keep Antipa ex- that to be included in the mix as a firm as

Winu is being lined up for production in posed to upside associated with green- a satellite pit.

2023, subject to necessary approvals. fields discoveries, while it continues “It’s also important to understand that

In tandem with building its inventory of apace at its 100%-owned Minyari-WACA we are not building a process plant, that

4.4 moz gold, 1.8mt copper and 35 moz (723,000oz @ 2 g/t gold, 26,000t @ is not part of our JV with Rio Tinto. We

silver at Winu, Rio Tinto will spend about 0.24% copper and 233,000oz silver @ will basically have a pit and a haul road,

$24.5 million on exploration at the Citadel 0.7 g/t) project. so there is nothing major to be keeping

JV with Antipa this year. Minyari is also considered a medium- up with.”

Rio Tinto’s graduation to 65% operating term production possibility and as ex- Newcrest has demonstrated at Telfer

interest, with potential to increase another ploration continues down-dip evidence that challenges associated with operat-

10% through further expenditure commit- mounts that the project bears similarities ing in the Paterson Province aren’t insur-

ments, spurred Antipa into a capital rais- to the nearby Newcrest/Greatland Gold mountable and with the tailwinds in both

ing last month – $22 million institutional plc Havieron project. the copper and gold sectors not expected

placement and $3 million SPP – to fund On top of a 21,000m RC and diamond to dissipate anytime soon, the region is

its share. drilling programme targeting extensions thriving, Power said.

Antipa’s largest shareholders, New- to the Minyari, WACA and Judes depos- “Generally, there is a lot of activity up

crest Mining Ltd (9.9%), and IGO Ltd its, Antipa will carry out mining and geo- there and there is obvious competition

(4.9%) supported the raising to maintain technical studies as part of project devel- for equipment and personnel, but nothing

their positions in the company, while ex- opment work. that is going to interfere with what we are

ecutive chairman Stephen Power report- While Antipa ups the ante at Minyari, trying to achieve,” Power said.

ed widespread interest in the two-times Rio Tinto will proceed down the develop- “We have been up there a long time

oversubscribed placement. ment path at Winu and set up the next – 10 years – so we understand the area

“It has taken us a little while, but we are cab off the rank in Calibre. and our internal knowledge base would

right where we want to be in what will be “Winu has an oxide blanket over the be equal to anyone. Essentially it is all

a pivotal year in the company’s history,” top whereas Calibre is straight into fresh covered ground with desert sands but

Power told Paydirt. rock, there are no treatment problems, now you can look underneath. Impor-

The short to medium term outlook for and the grade is better which is impor- tantly, you haven’t got any false leads.

Antipa is bright with Rio Tinto forging tant to start up an operation with when Sometimes there are sulphides and other

ahead at Citadel, where the 1.3 moz gold, recouping your capex,” Power said. issues which give you false readings or

69,500t copper and 730,000oz Calibre “Plus, Calibre is not as deep, 70m be- false positives in your surveys – none of

silver project is the focus, while Newcrest low the surface, it is free dig, so it has a that applies to us. It is very bland geo-

and IGO are farming into the Wilki and number of advantages. It is good, and we physically.”

Paterson projects respectively. think there are reasonable prospects for – Mark Andrews

aUSTRaLIa’S PaYDIRT JUNe 2021 Page 33