Page 106 - Account 10

P. 106

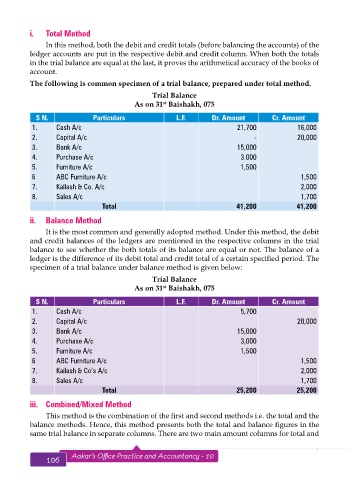

i. Total Method

In this method, both the debit and credit totals (before balancing the accounts) of the

ledger accounts are put in the respective debit and credit column. When both the totals

in the trial balance are equal at the last, it proves the arithmetical accuracy of the books of

account.

The following is common specimen of a trial balance, prepared under total method.

Trial Balance

As on 31 Baishakh, 075

st

S N. Particulars L.F. Dr. Amount Cr. Amount

1. Cash A/c 21,700 16,000

2. Capital A/c - 20,000

3. Bank A/c 15,000

4. Purchase A/c 3.000

5. Furniture A/c 1,500

6 ABC Furniture A/c 1,500

7. Kailash & Co. A/c 2,000

8. Sales A/c 1,700

Total 41,200 41,200

ii. Balance Method

It is the most common and generally adopted method. Under this method, the debit

and credit balances of the ledgers are mentioned in the respective columns in the trial

balance to see whether the both totals of its balance are equal or not. The balance of a

ledger is the difference of its debit total and credit total of a certain specified period. The

specimen of a trial balance under balance method is given below:

Trial Balance

As on 31 Baishakh, 075

st

S N. Particulars L.F. Dr. Amount Cr. Amount

1. Cash A/c 5,700

2. Capital A/c 20,000

3. Bank A/c 15,000

4. Purchase A/c 3,000

5. Furniture A/c 1,500

6 ABC Furniture A/c 1,500

7. Kailash & Co’s A/c 2,000

8. Sales A/c 1,700

Total 25,200 25,200

iii. Combined/Mixed Method

This method is the combination of the first and second methods i.e. the total and the

balance methods. Hence, this method presents both the total and balance figures in the

same trial balance in separate columns. There are two main amount columns for total and

106 Aakar’s Office Practice and Accountancy - 10 Trial Balance 107