Page 173 - Office Practice and Accounting -9

P. 173

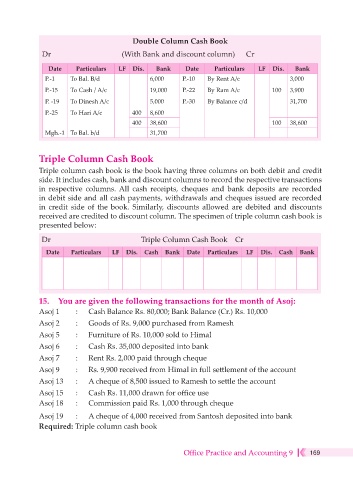

Double Column Cash Book

Dr (With Bank and discount column) Cr

Date Particulars LF Dis. Bank Date Particulars LF Dis. Bank

P.-1 To Bal. B/d 6,000 P.-10 By Rent A/c 3,000

P.-15 To Cash / A/c 19,000 P.-22 By Ram A/c 100 3,900

P. -19 To Dinesh A/c 5,000 P.-30 By Balance c/d 31,700

P.-25 To Hari A/c 400 8,600

400 38,600 100 38,600

Mgh.-1 To Bal. b/d 31,700

Triple Column Cash Book

Triple column cash book is the book having three columns on both debit and credit

side. It includes cash, bank and discount columns to record the respective transactions

in respective columns. All cash receipts, cheques and bank deposits are recorded

in debit side and all cash payments, withdrawals and cheques issued are recorded

in credit side of the book. Similarly, discounts allowed are debited and discounts

received are credited to discount column. The specimen of triple column cash book is

presented below:

Dr Triple Column Cash Book Cr

Date Particulars LF Dis. Cash Bank Date Particulars LF Dis. Cash Bank

15. You are given the following transactions for the month of Asoj:

Asoj 1 : Cash Balance Rs. 80,000; Bank Balance (Cr.) Rs. 10,000

Asoj 2 : Goods of Rs. 9,000 purchased from Ramesh

Asoj 5 : Furniture of Rs. 10,000 sold to Himal

Asoj 6 : Cash Rs. 35,000 deposited into bank

Asoj 7 : Rent Rs. 2,000 paid through cheque

Asoj 9 : Rs. 9,900 received from Himal in full settlement of the account

Asoj 13 : A cheque of 8,500 issued to Ramesh to settle the account

Asoj 15 : Cash Rs. 11,000 drawn for office use

Asoj 18 : Commission paid Rs. 1,000 through cheque

Asoj 19 : A cheque of 4,000 received from Santosh deposited into bank

Required: Triple column cash book

Office Practice and Accounting 9 169