Page 171 - Office Practice and Accounting -9

P. 171

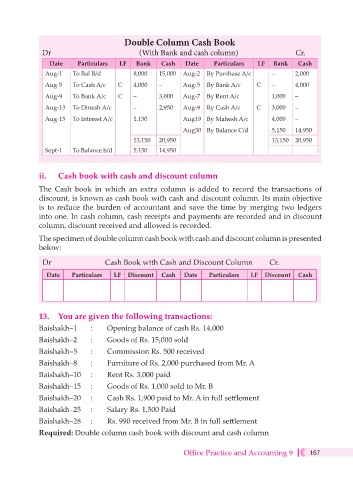

Double Column Cash Book

Dr (With Bank and cash column) Cr.

Date Particulars LF Bank Cash Date Particulars LF Bank Cash

Aug-1 To Bal B/d 8,000 15,000 Aug-2 By Purchase A/c – 2,000

Aug-5 To Cash A/c C 4,000 – Aug-5 By Bank A/c C – 4,000

Aug-9 To Bank A/c C – 3,000 Aug-7 By Rent A/c 1,000 –

Aug-13 To Dinesh A/c – 2,950 Aug-9 By Cash A/c C 3,000 –

Aug-15 To Interest A/c 1,150 Aug19 By Mahesh A/c 4,000 –

Aug30 By Balance C/d 5,150 14,950

13,150 20,950 13,150 20,950

Sept-1 To Balance b/d 5,150 14,950

ii. Cash book with cash and discount column

The Cash book in which an extra column is added to record the transactions of

discount, is known as cash book with cash and discount column. Its main objective

is to reduce the burden of accountant and save the time by merging two ledgers

into one. In cash column, cash receipts and payments are recorded and in discount

column, discount received and allowed is recorded.

The specimen of double column cash book with cash and discount column is presented

below:

Dr Cash Book with Cash and Discount Column Cr.

Date Particulars LF Discount Cash Date Particulars LF Discount Cash

13. You are given the following transactions:

Baishakh–1 : Opening balance of cash Rs. 14,000

Baishakh–2 : Goods of Rs. 15,000 sold

Baishakh–5 : Commission Rs. 500 received

Baishakh–8 : Furniture of Rs. 2,000 purchased from Mr. A

Baishakh–10 : Rent Rs. 3,000 paid

Baishakh–15 : Goods of Rs. 1,000 sold to Mr. B

Baishakh–20 : Cash Rs. 1,900 paid to Mr. A in full settlement

Baishakh–25 : Salary Rs. 1,500 Paid

Baishakh–28 : Rs. 990 received from Mr. B in full settlement

Required: Double column cash book with discount and cash column

Office Practice and Accounting 9 167