Page 691 - ANC20-Proceedings-Presentations-Full

P. 691

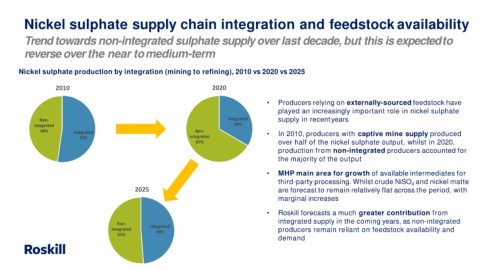

Nickel sulphate supply chain integration and feedstock availability

Trend towards non-integrated sulphate supply over last decade, but this is expectedto

reverse over the near tomedium-term

Nickel sulphate production by integration (mining to refining), 2010 vs 2020 vs 2025

2010 2020

• Producers relying on externally-sourced feedstock have

played an increasingly important role in nickel sulphate

Non- Integrated supply in recentyears

integrated 33%

48% Integrated Non- • In 2010, producers with captive mine supply produced

52% integrated

67% over half of the nickel sulphate output, whilst in 2020,

production from non-integrated producers accounted for

the majority of the output

• MHP main area for growth of available intermediates for

third-party processing. Whilst crude NiSO and nickel matte

4

2025 are forecast to remain relatively flat across the period, with

marginal increases

• Roskill forecasts a much greater contribution from

integrated supply in the coming years, as non-integrated

Non-

Integrated

integrated producers remain reliant on feedstock availability and

49%

51%

demand