Page 42 - 2021 Mid Year Open Enrollment Guide

P. 42

Income Protection Long-Term Disability

The Long-Term Disability (LTD) Plan is a fully-insured plan offered through Sun Life. Enrollment in

Basic Short-Term Disability the LTD plan is voluntary. The plan is designed to provide income protection to you during times of

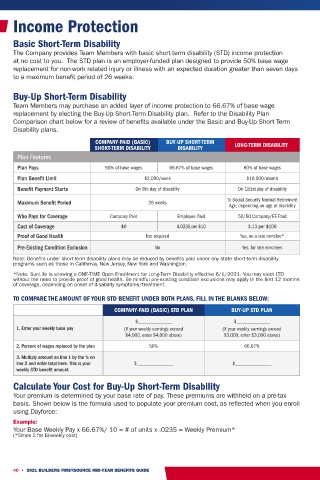

The Company provides Team Members with basic short-term disability (STD) income protection extended illness or injury over several months or even years, depending on your age at the onset

at no cost to you. The STD plan is an employer-funded plan designed to provide 50% base wage of disability. If you are receiving benefit payments under the STD plan, your claim will automatically

transition to Sun Life’s LTD claims unit as you near 180 days of disability. LTD benefits, once

replacement for non-work related injury or illness with an expected duration greater than seven days approved, begin on the 181st day of disability.

to a maximum benefit period of 26 weeks.

Refer to the Disability Plan Comparison chart on p. 40 for a review of both STD and LTD income

Buy-Up Short-Term Disability replacement plan provisions.

Team Members may purchase an added layer of income protection to 66.67% of base wage

replacement by electing the Buy-Up Short-Term Disability plan. Refer to the Disability Plan Cost of LTD Coverage

Comparison chart below for a review of benefits available under the Basic and Buy-Up Short Term The Company shares equally the cost of LTD coverage with you. As of 6/1/2021, the rates have

Disability plans. decreased to $.13/$100 of covered earnings. Your premium cost is determined on your base rate

COMPANY-PAID (BASIC) BUY-UP SHORT-TERM of pay. These premiums are withheld on an after-tax basis. When using Dayforce to review and/or

SHORT-TERM DISABILITY DISABILITY LONG-TERM DISABILITY elect coverage, your cost of coverage is automatically populated. To manually calculate your cost of

Plan Features coverage, you may use this formula to calculate your cost for the LTD coverage:

Plan Pays 50% of base wages 66.67% of base wages 60% of base wages

Example:

Plan Benefit Limit $2,000/week $10,000/month Your Base Monthly Pay / 100 = __________ # of Units x .13 = Monthly Premium

Benefit Payment Starts On 8th day of disability On 181st day of disability Then, Monthly Premium x 12 / __________ * Pay Periods = Per Paycheck

(*26 if paid Bi-Weekly or 52 if paid Weekly)

Maximum Benefit Period 26 weeks To Social Security Normal Retirement

Age, depending on age at disability

Who Pays for Coverage Company Paid Employee Paid 50/50 Company/EE Paid Open Enrollment for LTD for 6/1/21!

Sun Life is allowing a special ONE-TIME Open Enrollment for LTD coverage as of 6/1/21. This is a

Cost of Coverage $0 $.0235 per $10 $.13 per $100

great opportunity to elect coverage in the LTD plan without the need to provide proof of good health!

Proof of Good Health Not required Yes, as a late enrollee* If you are an ongoing team member who failed to elect LTD coverage when you were first eligible or

Pre-Existing Condition Exclusion No Yes, for late enrollees you may have applied for coverage and been denied based on your health, this is your opportunity to

enroll. Don’t miss out! However, be mindful, if you are a late enrollee to the plan during this Open

Note: Benefits under short-term disability plans may be reduced by benefits paid under any state short-term disability

programs such as those in California, New Jersey, New York and Washington. Enrollment opportunity, plan exclusions relating to pre-existing conditions may apply to you in the

first year of coverage.

*Note: SunLife is allowing a ONE-TIME Open Enrollment for Long-Term Disability effective 6/1/2021. You may elect LTD

without the need to provide proof of good health. Be mindful pre-existing condition exclusions may apply in the first 12 months

of coverage, depending on onset of disability symptoms/treatment. Maximum LTD Benefit Period

AGE AT

PERIOD

TO COMPARE THE AMOUNT OF YOUR STD BENEFIT UNDER BOTH PLANS, FILL IN THE BLANKS BELOW: The Maximum Benefit Period defines the maximum length of time DISABILITY MAXIMUM BENEFIT

for which benefits are payable under the plan, provided you remain

COMPANY-PAID (BASIC) STD PLAN BUY-UP STD PLAN continuously disabled. The Maximum Benefit Period most typically < 60 To SSNRA

$_____________ $_____________ pays until you reach Social Security Normal Retirement Age (SSNRA), 60 60 Months*

1. Enter your weekly base pay (If your weekly earnings exceed (If your weekly earnings exceed depending on your age at onset of disability, per the schedule here.

$4,000, enter $4,000 above) $3,000, enter $3,000 above) 61 48 Months*

How to Report a Disability Claim

2. Percent of wages replaced by the plan 50% 66.67% 62 42 Months*

Call Sun life at 833-812-5177. Please have this information handy:

3. Multiply amount on line 1 by the % on 63 36 Months*

line 2 and enter total here. This is your $______________ $______________ • Your name, address, phone number, birth date, date of hire,

weekly STD benefit amount. Social Security number 64 30 Months*

Calculate Your Cost for Buy-Up Short-Term Disability • Your employer’s name, address and phone number 65 24 Months*

Your premium is determined by your base rate of pay. These premiums are withheld on a pre-tax • Date of your claim and when you plan to return to work 66 21 Months*

basis. Shown below is the formula used to populate your premium cost, as reflected when you enroll • If you’re pregnant, give your expected delivery date 67 18 Months*

using Dayforce: • Name, address and phone number of each doctor you are seeing 68 15 Months*

Example: for this absence

Your Base Weekly Pay x 66.67%/ 10 = # of units x .0235 = Weekly Premium* 69+ 12 Months*

(*Times 2 for Bi-weekly cost) *or SSNRA, whichever

is longer

40 • 2021 BUILDERS FIRSTSOURCE MID-YEAR BENEFITS GUIDE 2021 BUILDERS FIRSTSOURCE MID-YEAR BENEFITS GUIDE • 41