Page 225 - Office Practice and Accounting 10

P. 225

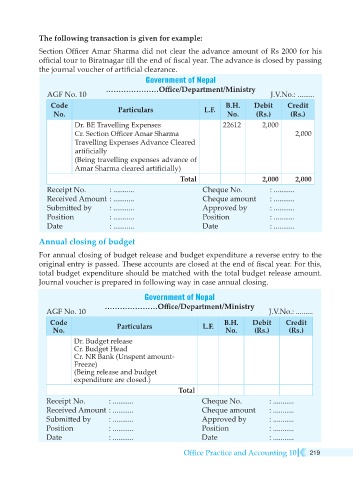

The following transaction is given for example:

Section Officer Amar Sharma did not clear the advance amount of Rs 2000 for his

official tour to Biratnagar till the end of fiscal year. The advance is closed by passing

the journal voucher of artificial clearance.

Government of Nepal

…………………Office/Department/Ministry

AGF No. 10 J.V.No.: .........

Code Particulars L.F. B.H. Debit Credit

No. No. (Rs.) (Rs.)

Dr. BE Travelling Expenses 22612 2,000

Cr. Section Officer Amar Sharma 2,000

Travelling Expenses Advance Cleared

artificially

(Being travelling expenses advance of

Amar Sharma cleared artificially)

Total 2,000 2,000

Receipt No. : ........... Cheque No. : ...........

Received Amount : ........... Cheque amount : ...........

Submitted by : ........... Approved by : ...........

Position : ........... Position : ...........

Date : ........... Date : ...........

Annual closing of budget

For annual closing of budget release and budget expenditure a reverse entry to the

original entry is passed. These accounts are closed at the end of fiscal year. For this,

total budget expenditure should be matched with the total budget release amount.

Journal voucher is prepared in following way in case annual closing.

Government of Nepal

…………………Office/Department/Ministry

AGF No. 10 J.V.No.: .........

Code B.H. Debit Credit

No. Particulars L.F. No. (Rs.) (Rs.)

Dr. Budget release

Cr. Budget Head

Cr. NR Bank (Unspent amount-

Freeze)

(Being release and budget

expenditure are closed.)

Total

Receipt No. : ........... Cheque No. : ...........

Received Amount : ........... Cheque amount : ...........

Submitted by : ........... Approved by : ...........

Position : ........... Position : ...........

Date : ........... Date : ...........

Office Practice and Accounting 10 219