Page 224 - Office Practice and Accounting 10

P. 224

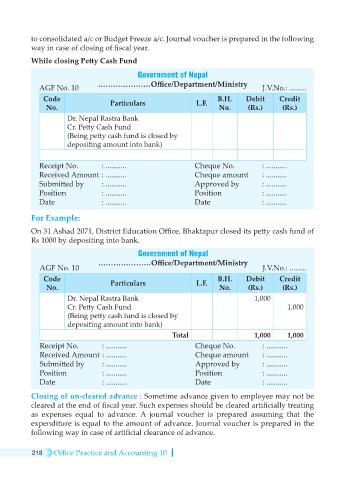

to consolidated a/c or Budget Freeze a/c. Journal voucher is prepared in the following

way in case of closing of fiscal year.

While closing Petty Cash Fund

Government of Nepal

AGF No. 10 …………………Office/Department/Ministry J.V.No.: .........

Code Particulars L.F. B.H. Debit Credit

No. No. (Rs.) (Rs.)

Dr. Nepal Rastra Bank

Cr. Petty Cash Fund

(Being petty cash fund is closed by

depositing amount into bank)

Receipt No. : ........... Cheque No. : ...........

Received Amount : ........... Cheque amount : ...........

Submitted by : ........... Approved by : ...........

Position : ........... Position : ...........

Date : ........... Date : ...........

For Example:

On 31 Ashad 2071, District Education Office, Bhaktapur closed its petty cash fund of

Rs 1000 by depositing into bank.

Government of Nepal

…………………Office/Department/Ministry

AGF No. 10 J.V.No.: .........

Code B.H. Debit Credit

No. Particulars L.F. No. (Rs.) (Rs.)

Dr. Nepal Rastra Bank 1,000

Cr. Petty Cash Fund 1,000

(Being petty cash fund is closed by

depositing amount into bank)

Total 1,000 1,000

Receipt No. : ........... Cheque No. : ...........

Received Amount : ........... Cheque amount : ...........

Submitted by : ........... Approved by : ...........

Position : ........... Position : ...........

Date : ........... Date : ...........

Closing of un-cleared advance : Sometime advance given to employee may not be

cleared at the end of fiscal year. Such expenses should be cleared artificially treating

as expenses equal to advance. A journal voucher is prepared assuming that the

expenditure is equal to the amount of advance. Journal voucher is prepared in the

following way in case of artificial clearance of advance.

218 Office Practice and Accounting 10