Page 223 - Office Practice and Accounting 10

P. 223

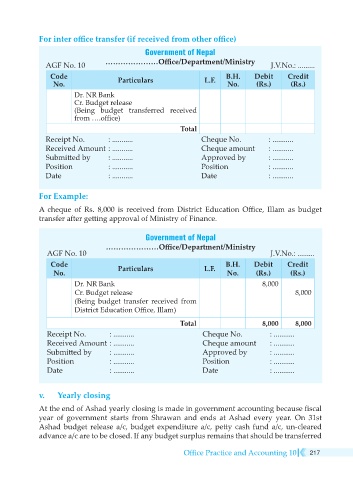

For inter office transfer (if received from other office)

Government of Nepal

AGF No. 10 …………………Office/Department/Ministry J.V.No.: .........

Code Particulars L.F. B.H. Debit Credit

No. No. (Rs.) (Rs.)

Dr. NR Bank

Cr. Budget release

(Being budget transferred received

from ….office)

Total

Receipt No. : ........... Cheque No. : ...........

Received Amount : ........... Cheque amount : ...........

Submitted by : ........... Approved by : ...........

Position : ........... Position : ...........

Date : ........... Date : ...........

For Example:

A cheque of Rs. 8,000 is received from District Education Office, Illam as budget

transfer after getting approval of Ministry of Finance.

Government of Nepal

…………………Office/Department/Ministry

AGF No. 10 J.V.No.: .........

Code B.H. Debit Credit

No. Particulars L.F. No. (Rs.) (Rs.)

Dr. NR Bank 8,000

Cr. Budget release 8,000

(Being budget transfer received from

District Education Office, Illam)

Total 8,000 8,000

Receipt No. : ........... Cheque No. : ...........

Received Amount : ........... Cheque amount : ...........

Submitted by : ........... Approved by : ...........

Position : ........... Position : ...........

Date : ........... Date : ...........

v. Yearly closing

At the end of Ashad yearly closing is made in government accounting because fiscal

year of government starts from Shrawan and ends at Ashad every year. On 31st

Ashad budget release a/c, budget expenditure a/c, petty cash fund a/c, un-cleared

advance a/c are to be closed. If any budget surplus remains that should be transferred

Office Practice and Accounting 10 217