Page 279 - Office Practice and Accounting 10

P. 279

budget release up to the current month, the amount of budget release of each column

is totaled and added with the total of the budget release received till the last month.

Yearly or Annual Closing : The process of closing budget sheet at the end of the

fiscal year is called annual closing. For closing the budget sheet, the total amount

of budget release and total amount of budget expenditure during the fiscal year are

totaled. The surplus amount, if any, is calculated by deducting budget expenditure

from budget release. The budget sheet is closed on the basis of journal voucher. The

surplus amount is either transferred to next year or to the budget freeze account or

deposited into the consolidated fund.

Illustrations

1. Consider the following transactions of a government office for the

month of Shrawan, 2071:

4 Shrawan, 2071 : Received a bank order letter for initial imprest fund Rs.4,00,000.

6 Shrawan, 2071 : Issued cheque no. 7676 of Rs. 1000 for the payment of office

material.

9 Shrawan, 2071 : Establishment of petty cash fund Rs. 500.

12 Shrawan, 2071 : Paid for furniture Rs. 10,000 through cheque no. 6767.

15 Shrawan, 2071 : Fuel expenses paid by cheque no 6876 Rs. 5,000.

19 Shrawan, 2071 : Paid house rent Rs. 8500 after deducting house rent tax 15% at

source.

22 Shrawan, 2071 : Cheque no. 6798 of Rs. 12,000 is issued to pay for staff dress.

28 Shrawan 2071 : Salary for the month Rs. 70,000 distributed after 10 % provident

fund deduction.

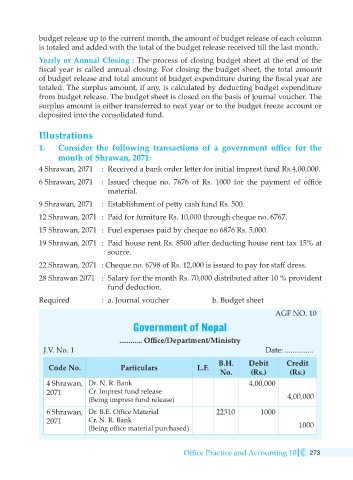

Required : a. Journal voucher b. Budget sheet

AGF NO. 10

Government of Nepal

............ Office/Department/Ministry

J.V. No. 1 Date: ...............

B.H. Debit Credit

Code No. Particulars L.F.

No. (Rs.) (Rs.)

4 Shrawan, Dr. N. R. Bank 4,00,000

2071 Cr. Imprest fund release

(Being imprest fund release) 4,00,000

6 Shrawan, Dr. B.E. Office Material 22310 1000

2071 Cr. N. R. Bank 1000

(Being office material purchased)

Office Practice and Accounting 10 273