Page 194 - Office Practice and Accounting 10

P. 194

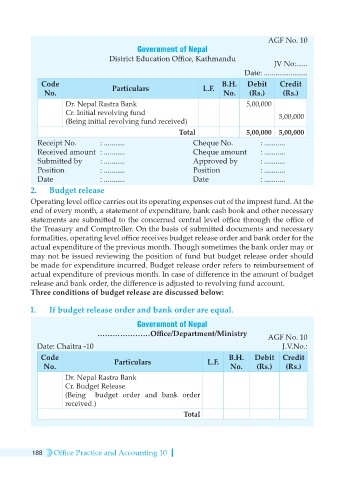

AGF No. 10

Government of Nepal

District Education Office, Kathmandu

JV No:......

Date: .......................

Code B.H. Debit Credit

No. Particulars L.F. No. (Rs.) (Rs.)

Dr. Nepal Rastra Bank 5,00,000

Cr. Initial revolving fund 5,00,000

(Being initial revolving fund received)

Total 5,00,000 5,00,000

Receipt No. : ........... Cheque No. : ...........

Received amount : ........... Cheque amount : ...........

Submitted by : ........... Approved by : ...........

Position : ........... Position : ...........

Date : ........... Date : ...........

2. Budget release

Operating level office carries out its operating expenses out of the imprest fund. At the

end of every month, a statement of expenditure, bank cash book and other necessary

statements are submitted to the concerned central level office through the office of

the Treasury and Comptroller. On the basis of submitted documents and necessary

formalities, operating level office receives budget release order and bank order for the

actual expenditure of the previous month. Though sometimes the bank order may or

may not be issued reviewing the position of fund but budget release order should

be made for expenditure incurred. Budget release order refers to reimbursement of

actual expenditure of previous month. In case of difference in the amount of budget

release and bank order, the difference is adjusted to revolving fund account.

Three conditions of budget release are discussed below:

I. If budget release order and bank order are equal.

Government of Nepal

…………………Office/Department/Ministry AGF No. 10

Date: Chaitra -10 J.V.No.:

Code B.H. Debit Credit

No. Particulars L.F. No. (Rs.) (Rs.)

Dr. Nepal Rastra Bank

Cr. Budget Release

(Being budget order and bank order

received.)

Total

188 Office Practice and Accounting 10