Page 261 - Office Practice and Accounting 10

P. 261

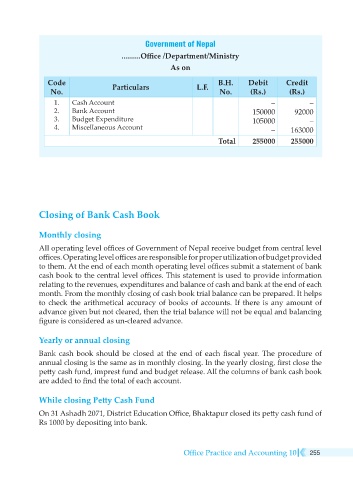

Government of Nepal

..........Office /Department/Ministry

As on

Code B.H. Debit Credit

No. Particulars L.F. No. (Rs.) (Rs.)

1. Cash Account – –

2. Bank Account 150000 92000

3. Budget Expenditure 105000 –

4. Miscellaneous Account – 163000

Total 255000 255000

Closing of Bank Cash Book

Monthly closing

All operating level offices of Government of Nepal receive budget from central level

offices. Operating level offices are responsible for proper utilization of budget provided

to them. At the end of each month operating level offices submit a statement of bank

cash book to the central level offices. This statement is used to provide information

relating to the revenues, expenditures and balance of cash and bank at the end of each

month. From the monthly closing of cash book trial balance can be prepared. It helps

to check the arithmetical accuracy of books of accounts. If there is any amount of

advance given but not cleared, then the trial balance will not be equal and balancing

figure is considered as un-cleared advance.

Yearly or annual closing

Bank cash book should be closed at the end of each fiscal year. The procedure of

annual closing is the same as in monthly closing. In the yearly closing, first close the

petty cash fund, imprest fund and budget release. All the columns of bank cash book

are added to find the total of each account.

While closing Petty Cash Fund

On 31 Ashadh 2071, District Education Office, Bhaktapur closed its petty cash fund of

Rs 1000 by depositing into bank.

Office Practice and Accounting 10 255