Page 129 - (DK) The Business Book

P. 129

MAKING MONEY WORK 127

See also: Accountability and governance 130–31 ■ Who bears the risk? 138–45 John Kay

■ Ignoring the herd 146–49 ■ Profit versus cash flow 152–53

Professor John Kay is a British

economist born in 1948. Best

known for his sceptical support

for free-market business

behavior, he is a visiting

professor at the London School

of Economics and regular

contributor to the Financial

Times. In 2012 he presented

a detailed report to the UK

government on the stock

market, which emphasized

that the normal purpose

of stock markets is not

speculation, but to provide

companies with access to

capital and to provide savers

with an opportunity to share

in economic growth. He also

highlighted concern about

excess dividend payouts.

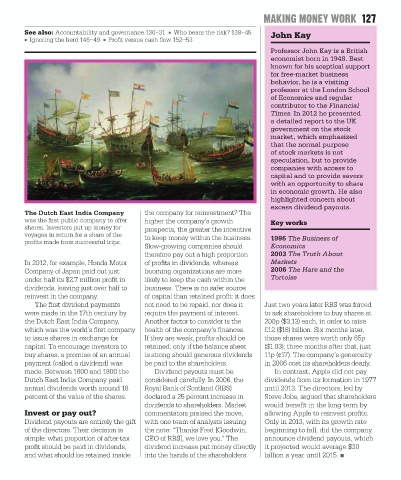

The Dutch East India Company the company for reinvestment? The

was the first public company to offer higher the company’s growth Key works

shares. Investors put up money for prospects, the greater the incentive

voyages in return for a share of the to keep money within the business. 1996 The Business of

profits made from successful trips.

Slow-growing companies should Economics

therefore pay out a high proportion 2003 The Truth About

In 2012, for example, Honda Motor of profits in dividends, whereas Markets

Company of Japan paid out just booming organizations are more 2006 The Hare and the

under half its $2.7 million profit in likely to keep the cash within the Tortoise

dividends, leaving just over half to business. There is no safer source

reinvest in the company. of capital than retained profit: it does

The first dividend payments not need to be repaid, nor does it Just two years later RBS was forced

were made in the 17th century by require the payment of interest. to ask shareholders to buy shares at

the Dutch East India Company, Another factor to consider is the 200p ($3.13) each, in order to raise

which was the world’s first company health of the company’s finances. £12 ($18) billion. Six months later,

to issue shares in exchange for If they are weak, profits should be those shares were worth only 65p

capital. To encourage investors to retained; only if the balance sheet ($1.03); three months after that, just

buy shares, a promise of an annual is strong should generous dividends 11p (¢17). The company’s generosity

payment (called a dividend) was be paid to the shareholders. in 2006 cost its shareholders dearly.

made. Between 1600 and 1800 the Dividend payouts must be In contrast, Apple did not pay

Dutch East India Company paid considered carefully. In 2006, the dividends from its formation in 1977

annual dividends worth around 18 Royal Bank of Scotland (RBS) until 2013. The directors, led by

percent of the value of the shares. declared a 25 percent increase in Steve Jobs, argued that shareholders

dividends to shareholders. Market would benefit in the long term by

Invest or pay out? commentators praised the move, allowing Apple to reinvest profits.

Dividend payouts are entirely the gift with one team of analysts issuing Only in 2013, with its growth rate

of the directors. Their decision is the note: “Thanks Fred [Goodwin, beginning to fall, did the company

simple: what proportion of after-tax CEO of RBS], we love you.” The announce dividend payouts, which

profit should be paid in dividends, dividend increase put money directly it projected would average $30

and what should be retained inside into the hands of the shareholders. billion a year until 2015. ■