Page 292 - Office Practice and Accounting 10

P. 292

in their personal ledger to record every deposit and withdrawal of customer. The

bank cash book and bank statement record the same transactions, thus, the balance

disclosed by them must tally. But it very often happens that the bank balance as shown

by the cash book does not tally with the balance shown by the bank pass book. To find

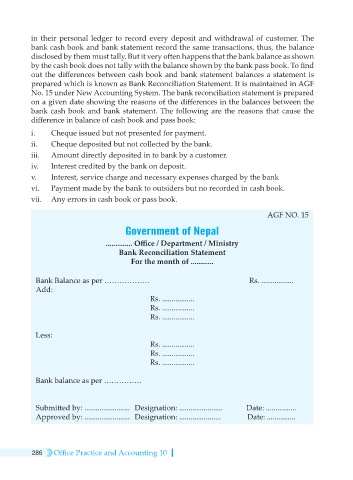

out the differences between cash book and bank statement balances a statement is

prepared which is known as Bank Reconciliation Statement. It is maintained in AGF

No. 15 under New Accounting System. The bank reconciliation statement is prepared

on a given date showing the reasons of the differences in the balances between the

bank cash book and bank statement. The following are the reasons that cause the

difference in balance of cash book and pass book:

i. Cheque issued but not presented for payment.

ii. Cheque deposited but not collected by the bank.

iii. Amount directly deposited in to bank by a customer.

iv. Interest credited by the bank on deposit.

v. Interest, service charge and necessary expenses charged by the bank

vi. Payment made by the bank to outsiders but no recorded in cash book.

vii. Any errors in cash book or pass book.

AGF NO. 15

Government of Nepal

.............. Office / Department / Ministry

Bank Reconciliation Statement

For the month of ............

Bank Balance as per ……………… Rs. .................

Add:

Rs. .................

Rs. .................

Rs. .................

Less:

Rs. .................

Rs. .................

Rs. .................

Bank balance as per ……………

Submitted by: ........................ Designation: ....................... Date: ................

Approved by: ........................ Designation: ...................... Date: ...............

286 Office Practice and Accounting 10