Page 126 - Office Practice and Accounting -9

P. 126

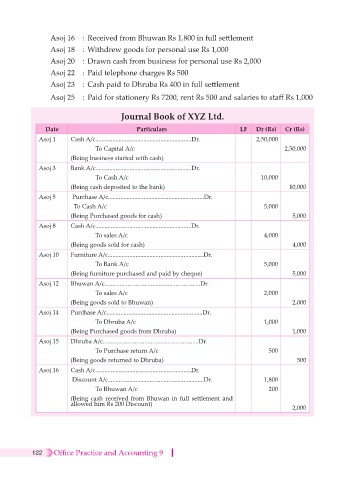

Asoj 16 : Received from Bhuwan Rs 1,800 in full settlement

Asoj 18 : Withdrew goods for personal use Rs 1,000

Asoj 20 : Drawn cash from business for personal use Rs 2,000

Asoj 22 : Paid telephone charges Rs 500

Asoj 23 : Cash paid to Dhruba Rs 400 in full settlement

Asoj 25 : Paid for stationery Rs 7200, rent Rs 500 and salaries to staff Rs 1,000

Journal Book of XYZ Ltd.

Date Particulars LF Dr (Rs) Cr (Rs)

Asoj 1 Cash A/c ..............................................................Dr. 2,50,000

To Capital A/c 2,50,000

(Being business started with cash)

Asoj 3 Bank A/c..............................................................Dr.

To Cash A/c 10,000

(Being cash deposited to the bank) 10,000

Asoj 5 Purchase A/c..............................................................Dr.

To Cash A/c 5,000

(Being Purchased goods for cash) 5,000

Asoj 8 Cash A/c..............................................................Dr.

To sales A/c 4,000

(Being goods sold for cash) 4,000

Asoj 10 Furniture A/c..............................................................Dr.

To Bank A/c 5,000

(Being furniture purchased and paid by cheque) 5,000

Asoj 12 Bhuwan A/c..............................................................Dr.

To sales A/c 2,000

(Being goods sold to Bhuwan) 2,000

Asoj 14 Purchase A/c..............................................................Dr.

To Dhruba A/c 1,000

(Being Purchased goods from Dhruba) 1,000

Asoj 15 Dhruba A/c..............................................................Dr.

To Purchase return A/c 500

(Being goods returned to Dhruba) 500

Asoj 16 Cash A/c..............................................................Dr.

Discount A/c..............................................................Dr. 1,800

To Bhuwan A/c 200

(Being cash received from Bhuwan in full settlement and

allowed him Rs 200 Discount)

2,000

122 Office Practice and Accounting 9